About What Health Insurance Should I Get

Alternatively, depending upon your age and health, you may have the ability to get a whole life policy by filling out a medical survey. If you pass the questions, some life insurance coverage companies will provide the policy without the need for a medical test. This is called streamlined concern or streamlined underwriting. Simplified issue makes it convenient and quick to apply for insurance. But if best place to buy a timeshare you're healthy, you can get a better rate by taking the medical examination and getting full medical underwriting. Entire life insurance coverage is special because part of your premium enters into a tax-deferred cost savings part understood as the policy's "cash worth." This quantity is normally guaranteed to grow in time at a minimum rate of returnperhaps around 3% -4% overallwithout decreasing.

Here's how it works. When you've paid into your life insurance policy for a long time (generally at least 2 to five years), the money worth accumulation will be enough for you to obtain tax-free, with the best planningalthough you'll pay interest, much like you do with any other kind of timeshare explained loan. And if you obtain and do not pay back, the quantity may be deducted from the survivor benefit. The accumulated money value might also pay your premiums in later years, and some policies even let you You can find out more put it towards a higher survivor benefit. However to access the entire cash worth, you might require to surrender the policy.

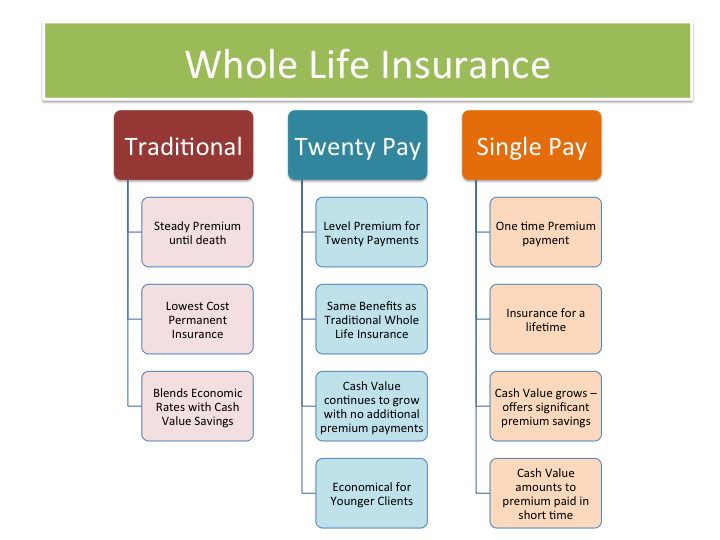

You might pay a "surrender charge" as a charge, as well. Upon your death, your life insurance policy keeps your accumulated money worth and only pays the death advantage. It may be paid as a lump amount, interest only, or in smaller installations (What is pmi insurance). In many cases, if you wish to leave a million dollars to your kids, an insurance coverage strategy's survivor benefit isn't considered gross income for the individual getting it, whether in a term insurance plan or entire life insurance. The majority of whole life policies have the very same goalto offer insurance coverage for your whole life. However, there are several types of whole life policies you may experience.

A Biased View of How Much Do Prescription Drugs Cost Without Insurance?

The dividends the business pays are based upon the insurer's yearly earnings, which might differ. Nonparticipating plans don't provide dividends. How much is renters insurance.: Protection is usually limited (generally to $25,000 however in some cases up to $50,000) however it does not need a medical examination. This is potentially practical if you have health concerns or are a senior trying to find life insurance coverage Guaranteed entire life is also a kind of insurance called last expense or burial insurance coverage.: These are low-cost policies developed for children. Age ranges vary, with many policies only available to kids 17 and under, though some are readily available into the applicant's 20s.

Within the buckets of getting involved and nonparticipating entire life plans, you might also come across options dealing primarily with payment structurewhich might be crucial thinking about the expenses involved.: Unlike many other entire life strategies, the premiums for this type of policy might change, though they won't exceed a guaranteed maximum.: Premiums (generally higher) are paid over a shorter duration of time.: Premium is paid as one upfront payment. Whole life may be an excellent suitable for those who desire long-lasting protection, have steady cash flow to regularly pay premiums, and have an appropriate emergency fund and routine retirement contributions underway.

Whole life might not be an excellent suitable for those with temporary insurance needs, those with limited spending plans, or those who don't want the entire life insurance cash worth technique to cost savings. For an option, examine term insurance plus investing in risk-appropriate vehicles, including tax-deferred pension, low-cost index funds, bonds, and other alternatives. Single individuals with no children typically do not need any kind of life insurance coverage at all. Rates will vary depending on your age, health, policy term, protection features, and the life insurance coverage company you select. Similar to other types of insurance, costs may also change if you include riders, such as a premium waiver if you end up being disabled, or the ability to contribute to the survivor benefit later without taking a medical examination (ensured insurability).

Fascination About What Is Liability Insurance

Examples of Whole Life Insurance Month-to-month Rates for Ladies Age $250,000 $500,000 $1,000,000 30 $227 $448 $888 40 $325 $643 $1,278 50 $484 $960 $1,914 Source: Quotacy Examples of Whole Life Insurance Month-to-month Rates for Men Age $250,000 $500,000 $1,000,000 30 $259 $511 $1,015 40 $374 $741 $1,477 50 $567 $1,128 $2,249 Source: Quotacy Whole life is 6 to 10 times more pricey than term life, however offers lifetime protection Whole life insurance coverage offers a death advantage, a "money value" portion that imitates tax-free cost savings, and in many cases, dividends Entire life policies are readily available with or without a medical examination Taking a medical examination can decrease your costs if you are healthy Set payment premiums can help you spending plan The Balance does not supply tax, investment, or monetary services and advice.

Entire life insurance is a great way to protect your household's future while likewise collecting money worth, which can help you throughout your life. Entire life insurance coverage is a kind of permanent life insurance, which implies it does not have an end date it covers you for your whole life. In contrast, term life insurance coverage ends after a certain variety of years and does not accumulate cash worth. With entire life insurance, as you pay premiums, your policy develops equity, which is your built up money value. This money can be utilized whenever, and for any factor be it to spend for a kid's wedding event, to redesign your home, to begin a service or to assist supplement retirement earnings.

Here's how entire life insurance coverage works. Whole life insurance doesn't have a term; that is, it covers you for your whole life. As long as you pay your premiums, your death advantage is guaranteed for life, generally tax-free, no matter when you pass away. With whole life insurance coverage, your premiums will remain the very same up until you have completed spending for your policy, either when you get to a specific age or after a set number of years (How much is renters insurance). When you end up paying premiums on an entire life insurance coverage policy, your protection will stay in place and you will not owe any more; it's sort of like paying off your home mortgage.

Everything about How To Become An Insurance Adjuster

If your policy has Mixed Term insurance coverage, there is an opportunity that additional premiums might be required in the future if there is a considerable drop in the dividend scale of the business. At Northwestern Mutual, the cost of our insurance coverage is based on certain assumptions, like how lots of death claims we expect to pay in a year. Whenever the business carries out better than we presumed, we might pay a dividend to our insurance policy holders (which we have actually done every year since 1872). With entire life insurance, you can utilize dividends to acquire paid-up insurance coverage, which can increase your survivor benefit and built up cash value faster than your policy's warranties.